ACH Processing

Automated Clearing House (ACH) is an electronic funds-transfer system that facilitates the transfer of funds directly between bank accounts. ACH payments are essentially electronic checks, also known as e-checks, that use the routing and account number of both parties to facilitate an electronic transfer between bank accounts. The ACH Network is governed by the National Automated Clearing House Association (NACHA) which sets rigorous standards for security and is the middle step of the transfer of funds.

Making a payment via the ACH network differs from making a payment with a credit card in that money is being sent directly from one account to another, instead of charging it to a card the end customer would later be liable to make a payment on. One other differentiator with ACH vs. credit card transactions is that customers cannot make ACH payments with international banking information at Stax, bank information used for ACH payments must be based in the United States.

Once a customer makes a payment via ACH, the sub-merchant will usually be funded in five (5) days*. This funding period is in place to help minimize the number of clawbacks that can occur. During this period of time, the funds are traveling through the ACH networks and Stax’s systems are waiting for the banks to provide an answer as to the ability to debit the customer’s account. Most banks will provide an answer within this period of time as to the ability to debit the customer’s account and once that level of certainty is reached, the sub-merchant will be funded and the ability to refund a transaction is available.

Although most banks will provide an answer within this period of time, banks are not required to reply during this period and in most cases it could take up to ten (10) business days to receive a response on the success of a transaction. Stax automatically funds all ACH transactions before this 10 day period in “good faith”, assuming that the sub-merchant has the available funds to cover if needed. As a best practice, it is recommended to wait between 7-10 days before initiating a refund to be certain the transaction was fully funded and avoid a duplicate credit to the end customer.

ACH Transaction Lifecycle

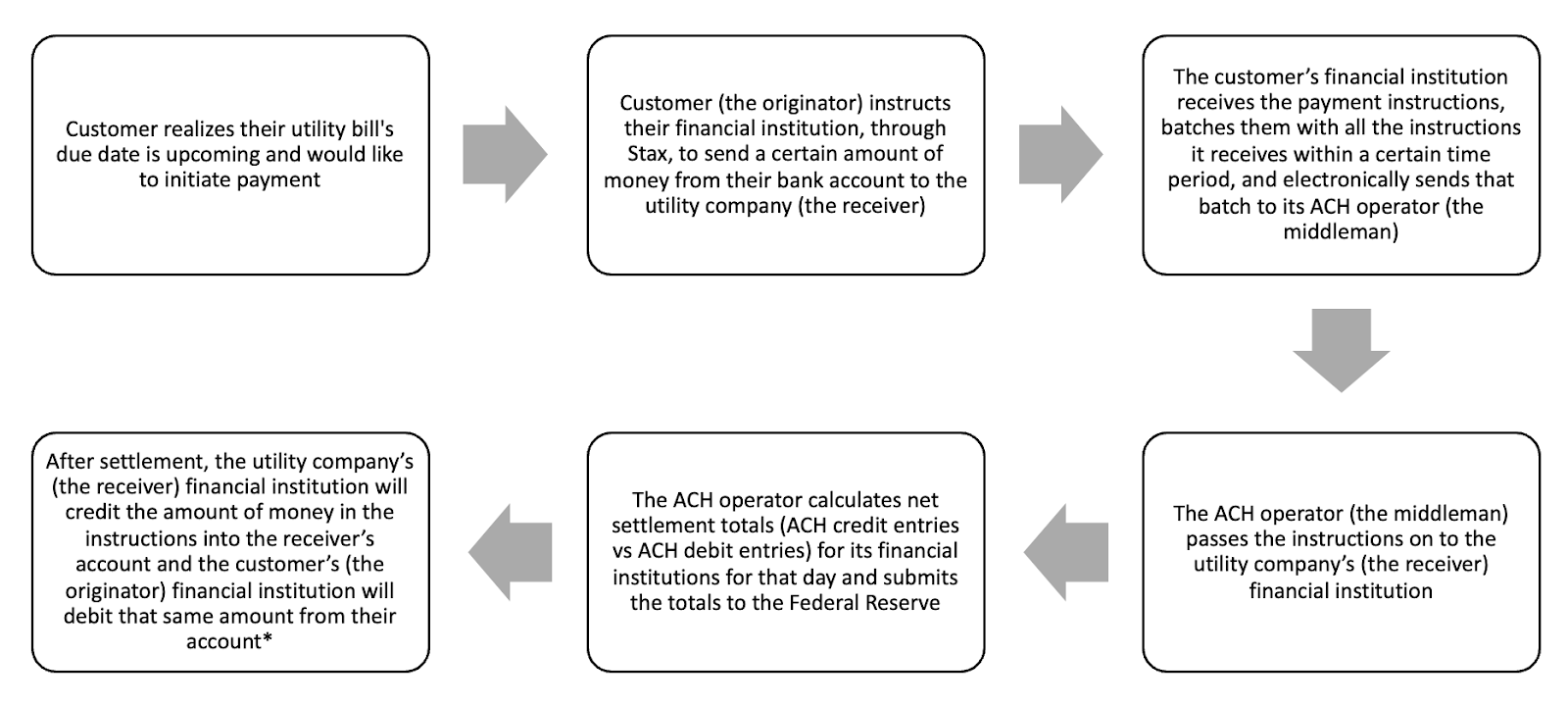

To send money through the ACH Network, a business or individual initiates an ACH credit entry. This process enables the originator of the transaction to push money through the ACH Network to another bank account. Here’s an example of the lifecycle of an ACH transaction using the scenario of a customer initiating an ACH payment to their utility company:

*Note the timing of the debit from the originator’s account and the credit from the receiver’s account can vary based on the financial institution

The lifecycle of an ACH transaction can take up to 10 business days to fully settle, but Stax automatically funds all ACH transactions before this 10 day period in “good faith”, assuming that the sub-merchant has the available funds to cover if needed.

Refunds

There may be instances where the end customer has requested a refund on an ACH transaction. If this occurs it is important to note that Stax usually funds ACH transactions to the sub-merchant’s bank account in five (5) business days. Although ACH transactions are funded in 5 business days, they can actually take up to ten (10) business days to fully settle and clear through the Automated Clearing House Networks.

Due to this, Stax does not allow ACH refunds to be initiated until a minimum of 5 calendar days after a transaction has occurred. Best practice is to wait 7-10 days before a sub-merchant issues a refund in case of a clawback. Delaying the possibility of ACH refunds helps to mitigate against the possibility of double crediting an end customer who requested a refund for an ACH payment before it was cleared.

Updated 7 months ago