Interchange

When you research payment solution providers, you’ll start hearing the term “interchange” used when discussing payments. Interchange is the fee credit card companies like Visa and Mastercard charge businesses to accept their cards.

The interchange fee depends on several factors and isn’t always easy to understand. This article will break down credit card interchange fees so you will know exactly how much you’re spending when running your business.

Interchange Fees

Interchange is the fee credit card companies charge businesses to accept their cards. Essentially, the merchant pays the card brand for the convenience of accepting this payment method since that is how your customers want to pay.

Interchange fees help cover the risks associated with accepting electronic payments while ensuring your company has access to guaranteed payment when a customer makes a purchase. Interchange fees are simply a cost of doing business.

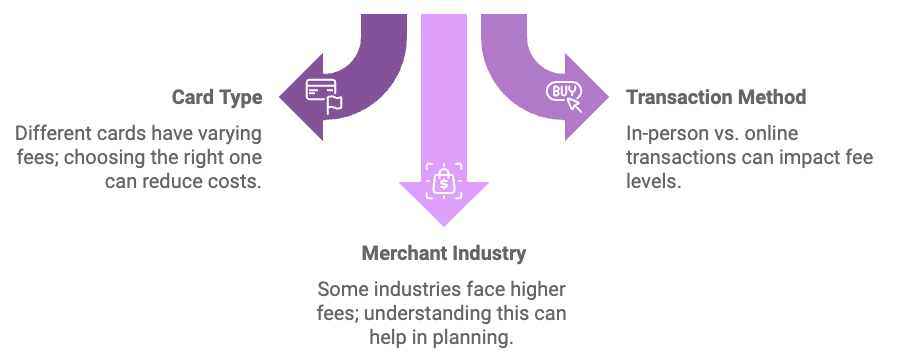

Understanding interchange fees is crucial for businesses looking to optimize their payment processing costs. The payment networks set these fees, typically expressed as a percentage of the transaction value or as a fixed amount per transaction. The fee structure varies depending on card type, transaction type, industry, and location.

It’s important to note that your payment processor or bank does not collect interchange fees; they go directly to the card-issuing banks. Your payment processor, however, facilitates the transaction and deducts its processing fee from the overall charge.

Debit card transactions generally have lower interchange fees compared to credit card transactions. This is because debit cards are linked directly to the customer’s bank account, and the risk of non-payment or default is lower. Businesses can effectively reduce the interchange fees associated with card payments by actively encouraging customers to use debit cards.

While interchange fees may seem like an added expense, it’s crucial to recognize the value they bring to your business. Accepting credit and debit cards allows you to cater to a wider customer base, improve customer satisfaction, and enhance the overall shopping experience. You can attract more customers and increase sales by offering convenient payment options.

To ensure reasonable and competitive interchange fees, it’s essential to regularly review and negotiate your fee structure with your payment processor. Stay informed about any updates or changes in interchange fee schedules to ensure you’re paying the most optimal rates for your business.

Optimizing your payment processing infrastructure and implementing measures to minimize chargebacks can significantly reduce interchange fees. Investing in secure payment gateways, fraud detection systems, and robust transaction processing protocols can lower the risk of chargebacks and avoid unnecessary fees.

Remember, while interchange fees are an inherent part of accepting card payments, implementing smart strategies and staying proactive can help minimize their impact on your business. One such strategy includes implementing credit card surcharging to offset the cost of interchange fees. By understanding the fee structure, promoting debit card usage, and optimizing your payment processing operations, you can effectively manage and reduce interchange fees, ultimately improving your bottom line.

Interchange fees are an essential consideration for businesses that accept card payments. These fees are a cost that businesses incur to facilitate the convenience and security of card transactions. While it’s true that businesses pay interchange fees, it’s important to understand that they are a necessary part of the payment ecosystem.

Interchange fees enable payment networks and card-issuing banks to cover the costs associated with maintaining the infrastructure, managing fraud risk, and providing the benefits and rewards programs associated with credit and debit cards.

As a business owner, it’s crucial to factor in these interchange fees when evaluating the overall costs of accepting card payments. By understanding the dynamics of interchange fees and implementing strategies to optimize their impact, businesses can effectively manage their expenses and find a balance that allows them to provide convenient payment options to customers while minimizing the amount they pay in interchange fees.

Interchange Cost

Interchange fees vary widely among card brands, credit card networks, card types, and card processing methods. Credit cards that offer points or rewards typically have higher interchange fees, as do corporate cards.

Generally, debit card transactions are much less expensive than credit card payments for you to process and come with a lower interchange rate than credit cards. Card-present transactions also incur lower rates compared to card-not-present transactions. However, an exemption to this is debit cards issued by a bank with less than $10 billion in assets, also referred to as “exempt,” often a local bank or credit union—these have some of the highest interchange rates.

While you can control whether a cardholder’s card is swiped or keyed in at the point of sale, you can’t control what card they use. That’s why interchange varies so widely. For a $100 transaction, a swiped Mastercard debit card will cost you around 27¢. However, using a Visa corporate commercial credit card will cost you around $2.60 for the same transaction. It’s easy to see how these fees can stack up over the year.

Avoiding Higher Interchange Fees

In the modern digital age, electronic payments have become the norm, with credit and debit cards being widely used for transactions. However, along with the convenience of card payments, businesses face the challenge of interchange fees, which can significantly impact their bottom line.

Choose the Right Payment Processor

The choice of payment processor plays a crucial role in managing interchange fees. Different processors offer various pricing models, so comparing options and negotiating competitive rates is essential. Look for processors that provide transparent pricing structures and offer interchange plus pricing, where the interchange fee is passed through directly without any markup. This approach can help you avoid additional charges and optimize your fee structure.

Optimize Card Acceptance

Understanding the types of cards you accept and their associated interchange fees is key to minimizing costs. Payment networks classify cards into different categories, and fees vary depending on factors like card type (credit or debit), payment method (chip and PIN, contactless), and industry-specific cards (corporate, rewards). By optimizing your card acceptance policies, you can encourage customers to use lower-cost payment methods and reduce interchange fees.

Encourage Debit Card Usage

Debit cards generally carry lower interchange fees compared to credit cards. Promoting debit card usage among customers can help lower your interchange fee expenses. Consider offering incentives, such as discounts or rewards, for customers who pay with debit cards. This not only benefits your customers but also reduces your payment processing costs.

Streamline Processing and Reduce Chargebacks

Efficient transaction processing and minimizing chargebacks can positively impact interchange fees. Implementing secure payment gateways and fraud detection systems can help reduce the risk of chargebacks, resulting in costly fees. Furthermore, optimizing your payment infrastructure to streamline processing and minimize errors can help prevent unnecessary charges and improve overall cost efficiency.

Regularly Review and Update Your Fee Structure

Interchange fees are subject to change as payment networks periodically update their fee schedules. It is crucial to stay informed about these changes and regularly review your fee structure to ensure you’re paying the most competitive rates available. This review process may involve renegotiating with your payment processor or exploring alternative options in the market to find the best fit for your business.

Consider Surcharge Programs

Depending on your region and applicable regulations, you can implement surcharge programs, where you pass on the interchange fees to customers directly. While this strategy requires careful consideration and compliance with legal requirements, it can effectively offset interchange fees (especially for small businesses) and transfer the cost to the end user.

Interchange fees are charges imposed by payment networks, such as Visa and Mastercard, for processing card transactions. While these fees are unavoidable, businesses can employ several smart strategies to minimize their impact. This article will explore practical tips to help businesses navigate and reduce interchange fees effectively.

Pricing Models

| Model | How it Works | Pros | Cons |

|---|---|---|---|

| Tiered | Categorized into 3 tiers | Lower for "qualified" | Lack of transparency |

| Flat Rate | Fixed percentage + fee | Simplicity | Potential overpayment |

| Subscription | Flat monthly fee | Predictable costs | Requires volume analysis |

Tiered Pricing

A common pricing model in payment processing is tiered pricing. This method bundles the interchange rate with the processor’s markup and divides transactions into three tiers: qualified, mid-qualified, and non-qualified.

Card payments in the “qualified” tier incur lower rates, while “non-qualified” transactions cost more.

Here’s where things get dicey: how transactions are categorized is completely at the processor's discretion. What some payment processing companies consider “qualified” may not be the same for others. Tiered pricing fees are not transparent, making determining whether you’re overpaying difficult.

Set Rate Processing aka Flat Fee Processing

With set-rate processing, you pay a non-negotiable flat fee per credit card transaction, regardless of card or industry type. For instance, Stripe charges 2.9% + 30¢ per transaction. So whether you accept a debit card with a 0.05% + 22¢ interchange rate or a corporate card with a 2.50% + 10¢ interchange rate, you pay the same rate.

While this may seem simpler at first, the reality is that you could be overpaying for credit card processing with these systems. In the example above, Visa would receive the .05% + 22¢, while Stripe would make a whopping 2.5% + 8¢ on your transaction. That’s why we introduced simple subscription-based pricing.

Flat Subscription Rate Processing

Subscription-based processors have a similar concept to other subscription services you’re used to, such as warehouse stores like Costco. You pay a low fee to access warehouse pricing on goods, where you can buy as much as you want with no cap on savings. Stax’s subscription pricing starts at just $99 per month. Regardless of whether your sale is $50 or $5,000, you pay the flat cost of processing without a percent markup.

Every business is different, so we don’t believe in one-size-fits-all solutions. Based on the types of cards your customers are using and your average transactions, we can show you exactly which type of plan makes sense for your business.

Updated 7 months ago